Financial Year-End Property Investment in Jakkur: Tax and Timing Benefits

Year end property investment tax benefits — Section 24 home loan benefit, March property investment Bangalore, and tax saving home loan Jakkur strategy.

Why the January to March Window Matters as Much as Festive

The Indian financial year ends on 31 March, which makes the January to March period the second consequential real estate buying window of the year after the September to November festive season. For salaried buyers and business owners thinking about their tax position, this window often determines whether a planned property purchase happens in the current financial year or rolls into the next one. Understanding the year end property investment tax benefits available before March 31 helps buyers structure their purchase to capture the deductions that the tax code provides for home loan interest, principal repayment, and stamp duty.

Section 24 Home Loan Benefit

The Section 24 home loan benefit allows a deduction of up to ₹2 lakh per financial year on the interest paid on a home loan for a self-occupied property, and unlimited interest deduction for a let-out (rented) property. For a ₹3 Cr home loan at typical interest rates, annual interest costs run ₹22 to ₹26 lakh in the early years of the loan — the ₹2 lakh deduction (self-occupied) reduces taxable income materially for buyers in the higher tax brackets. For investors planning to rent the property, the full interest deduction makes luxury real estate one of the more tax-efficient asset classes in the Indian portfolio. This is a central component of the year end property investment tax benefits structure.

Section 80C Principal Repayment and Stamp Duty

Section 80C of the Income Tax Act allows a deduction of up to ₹1.5 lakh per financial year on home loan principal repayment, stamp duty, and registration charges combined. For a property purchased in March 2027, the stamp duty and registration paid in that financial year (potentially ₹25 to ₹30 lakh on a ₹4 Cr property) substantially exceeds the ₹1.5 lakh cap — the full benefit is captured in a single financial year. Combined with the Section 24 interest deduction, this delivers meaningful first-year tax savings that improve the effective entry economics for a property purchased in the year-end window.

March Property Investment Bangalore — The Timing Discipline

March property investment Bangalore activity peaks in the last two weeks before the 31 March deadline as buyers race to complete registration within the current financial year. The festive season cycle (September to November) sets up the decision, and the financial year-end deadline determines when execution actually happens. Sub-registrar offices in Karnataka typically see longer queues in late March, which means buyers should not leave registration to the final week — submission should happen by mid-March to provide buffer for any documentation rework. The year end property investment tax benefits depend on registration completing before 31 March, so timing discipline matters.

Tax Saving Home Loan Jakkur — Structuring for Maximum Benefit

Tax saving home loan Jakkur structuring involves three decisions. First, joint loan with a co-applicant (spouse) doubles the Section 24 deduction limit to ₹4 lakh per year combined, provided both applicants have separate taxable incomes. Second, the loan tenure should be aligned to the buyer's holding plan — longer tenures front-load interest payments, which maximises the early-year deductions. Third, principal prepayment timing should be planned around the Section 80C cap — prepaying ₹1.5 lakh of principal in the first year captures the deduction, with additional prepayment optimisations possible across subsequent years. These structuring choices can meaningfully improve the after-tax cost of capital for luxury real estate.

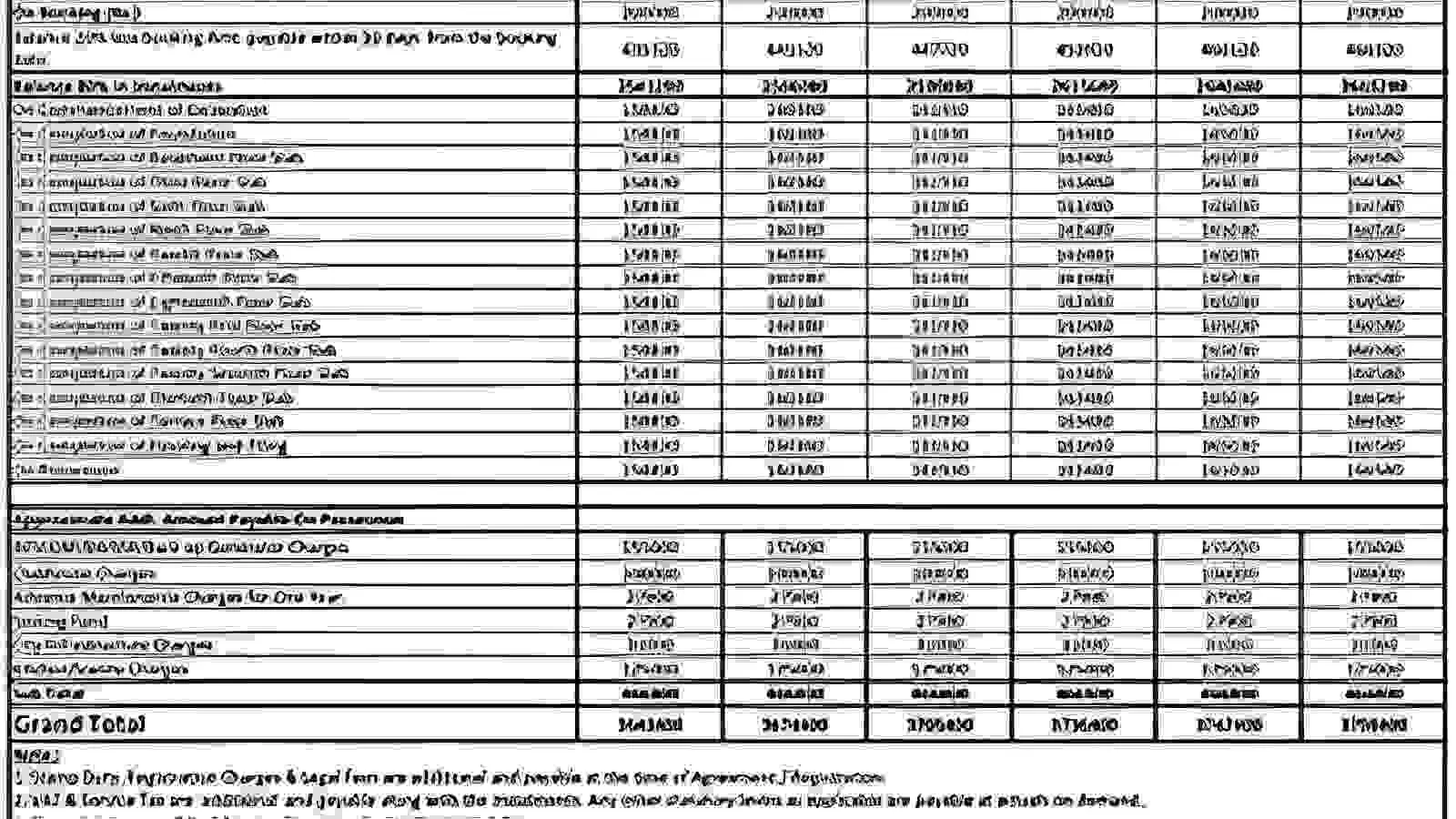

Indicative First-Year Tax Benefit (₹3 Cr Loan, Self-Occupied)

Deduction Category | Annual Amount | Tax Savings (30% bracket) |

|---|---|---|

Section 24 — Interest | ₹2,00,000 | ₹60,000 |

Section 80C — Principal | ₹1,50,000 | ₹45,000 |

Section 80C — Stamp Duty (FY of purchase) | Up to ₹1,50,000 | ₹45,000 |

Section 80EE / 80EEA (eligibility-dependent) | Up to ₹1,50,000 | Up to ₹45,000 |

Total Annual Tax Saving (Indicative) | — | ₹1,50,000 – 1,95,000 |

Why Investors Should Consider the Year-End Window

For salaried HNI buyers in the higher tax brackets, the year end property investment tax benefits are not the primary reason to buy a luxury home, but they meaningfully improve the after-tax economics. For business owners with discretion over income timing, the tax planning around a financial year-end purchase can be more substantial. For NRI buyers, the FY-end window also coincides with the Indian financial year tax-planning cycle for any income earned in India, which can support a coordinated approach to property purchase and tax filing. Each buyer profile should run their own numbers, but the window deserves attention.

Related reading: Balcony Planning, Ventilation and Natural Light in Luxury Apartments.

FAQs

What tax benefits are available for year-end property purchases?

Section 24 interest deduction up to ₹2 lakh annually (self-occupied) or unlimited (rented), Section 80C principal + stamp duty deduction up to ₹1.5 lakh annually, and additional first-year benefits.Why does March matter for property purchases?

Registration must complete before 31 March to claim the deductions in the current financial year. Sub-registrar offices in Karnataka see peak traffic in late March, so plan registration for mid-March.Can joint loans increase the tax benefit?

Yes. A joint loan with a spouse co-applicant doubles the Section 24 deduction limit to ₹4 lakh per year combined, provided both have separate taxable incomes.

Related Articles

Century Astoria Cost Sheet Explained: Complete Pricing Breakdown for 3 & 4 BHK

Decode the full Century Astoria cost sheet breakdown — base rate, PLC, GST, stamp duty and registration for 3 BHK and 4 BHK residences in Jakkur.

Century Astoria Payment Plans, Offers and Pre-Launch Benefits

Compare Century Astoria payment plan options — construction-linked, possession-linked, and customised schedules. See pre-launch booking benefits in Jakkur.

Century Astoria Possession Timeline: When Can You Move In?

Find out the Century Astoria possession date Jakkur — handover schedule, construction milestones, and what pre-launch to handover looks like for buyers.

Century Astoria Construction Updates and Quality Standards

Track Century Astoria construction quality — RCC structural framing, finishing standards, construction timeline, and quality control on the Jakkur project.