NRI investment guide Jakkur Bangalore — how NRIs can buy luxury apartments, NRI home loan, FEMA rules, repatriation, and step-by-step process for first.

Why Jakkur Sits on Most NRI Shortlists

Non-resident Indian buyers form a disproportionate share of the ultra-luxury Bangalore market — by some estimates, 25 to 35 percent of all transactions at the ₹3.5 Cr plus tier involve NRI capital. For this cohort, the NRI investment guide Jakkur Bangalore considerations are different from those of resident buyers, and getting the structure right at the outset prevents complications that can become expensive to unwind later. Jakkur sits on most NRI shortlists for three reasons — airport corridor proximity, the senior corporate housing demand base, and the height-protected long-term skyline.

How Can NRI Buy Apartment in Bangalore

How can NRI buy apartment in Bangalore is governed by the Foreign Exchange Management Act and the Reserve Bank of India's directives. The short answer is that NRIs and Persons of Indian Origin can purchase residential and commercial property in India without prior RBI approval, with limited exceptions for agricultural land, plantation property, and farmhouses. The transaction must use rupee funds — either remitted through banking channels into an NRE or NRO account, or held in existing Indian rupee accounts. Payment must be made through these channels rather than in foreign currency directly, which is why the NRI investment guide Jakkur Bangalore process begins with setting up the right banking infrastructure before transacting.

NRI Home Loan Jakkur — What Banks Will Finance

NRI home loan Jakkur availability is strong across all major Indian banks. Most banks will finance up to 80 percent of the property value for NRI buyers, with loan tenures up to 20 years and interest rates typically 25 to 50 basis points above resident borrower rates. Eligibility depends on overseas income documentation, employment stability, repayment capacity, and credit history both in India and the country of residence. Banks have developed specialised NRI desks that handle the documentation and processing remotely, with the loan agreement executed at the borrower's overseas location or through a Power of Attorney holder in India.

FEMA Rules for NRI Property Investment

FEMA rules for NRI property purchases govern three things — what can be bought, how payments must be routed, and how proceeds can be repatriated. NRIs can buy any number of residential or commercial properties without limit. Payments must come through NRE, NRO, or FCNR accounts via banking channels. Rental income can be credited to an NRE or NRO account, with NRE income freely repatriable and NRO income subject to a USD 1 million annual repatriation limit (covering both principal and rental income from up to two residential properties for principal repatriation). This NRI investment guide Jakkur Bangalore section is a summary — buyers should obtain country-specific tax advice based on their residence.

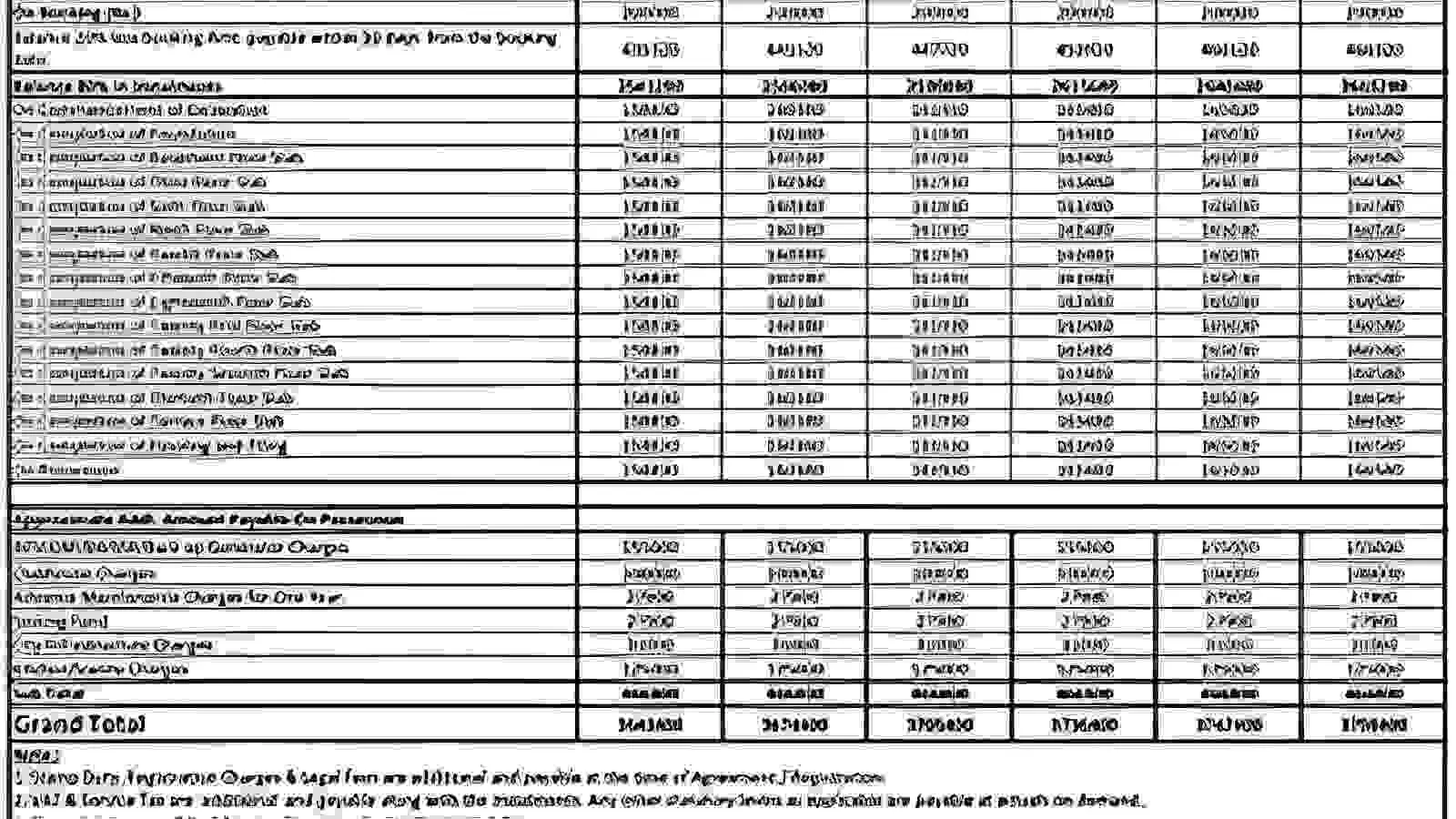

The Step-by-Step Purchase Process

The NRI purchase process for a Jakkur luxury apartment follows seven defined stages. Stage one is Expression of Interest and configuration selection, typically completed remotely via virtual site visit and document exchange. Stage two is the banking setup — opening an NRE/NRO account if not already in place, and arranging fund transfer. Stage three is the home loan application if financing is being used, with bank-side documentation handled in parallel. Stage four is the formal booking, executed either by the NRI in person or through a registered Power of Attorney holder in India. Stage five is the construction-linked payment schedule activation. Stage six is the agreement to sell registration with the Karnataka sub-registrar. Stage seven is possession handover and final payment.

Tax Implications for NRI Buyers

Three tax categories matter for NRI buyers. First, TDS at 1 percent on transactions above ₹50 lakh applies, with the buyer responsible for deducting at source on payments to the seller. Second, rental income is taxable in India under the Income Tax Act, with NRI sellers eligible for the same deductions as resident landlords (interest on home loan, municipal taxes, standard deduction for repairs). Third, capital gains on resale are taxable in India, with short-term gains (under 2 years holding) taxed at slab rates and long-term gains (over 2 years holding) taxed at 20 percent with indexation. Double Taxation Avoidance Agreement provisions may reduce home-country tax liability — country-specific advice is essential.

Indicative NRI Purchase Workflow

Stage | Typical Duration | Documentation Needed |

|---|---|---|

Expression of Interest | 1 – 2 weeks | Passport, OCI/PIO card, basic KYC |

Banking Setup | 2 – 4 weeks | NRE/NRO account opening, fund transfer |

Home Loan Application | 3 – 6 weeks | Overseas income proof, employment letter |

Formal Booking | 1 – 2 weeks | Booking agreement, payment receipt |

Sub-Registrar Registration | 2 – 4 weeks | Agreement to sell, stamp duty payment |

Construction Payments | Across 42 – 48 months | Per milestone schedule |

Possession Handover | 1 – 2 weeks | Final payment, occupancy certificate |

Related reading: Wellness Amenities in a Modern Luxury Apartment: A Complete Guide.

FAQs

Can NRIs buy luxury apartments in Bangalore?

Yes. NRIs and Persons of Indian Origin can purchase residential property in India without prior RBI approval, subject to FEMA payment routing requirements through NRE/NRO/FCNR accounts.What home loans are available for NRI buyers?

Most major Indian banks finance up to 80 percent of the property value for NRIs, with tenures up to 20 years. Specialised NRI desks handle remote documentation and processing.How is rental income from NRI-owned property taxed?

Rental income is taxable in India under the Income Tax Act. NRI landlords are eligible for the same deductions as residents (interest on home loan, municipal taxes, standard repair deduction).

Related Articles

Century Astoria Cost Sheet Explained: Complete Pricing Breakdown for 3 & 4 BHK

Decode the full Century Astoria cost sheet breakdown — base rate, PLC, GST, stamp duty and registration for 3 BHK and 4 BHK residences in Jakkur.

Century Astoria Payment Plans, Offers and Pre-Launch Benefits

Compare Century Astoria payment plan options — construction-linked, possession-linked, and customised schedules. See pre-launch booking benefits in Jakkur.

Century Astoria Possession Timeline: When Can You Move In?

Find out the Century Astoria possession date Jakkur — handover schedule, construction milestones, and what pre-launch to handover looks like for buyers.

Century Astoria Construction Updates and Quality Standards

Track Century Astoria construction quality — RCC structural framing, finishing standards, construction timeline, and quality control on the Jakkur project.